Prices and Coverages Are Set – Is Your APH Correct?

Now that we’re after the deadline for changes to crop insurance policies, there’s one area that often gets overlooked—the Actual Production History (APH), sometimes called your yield database. This is the foundation upon which your insurance coverage is built, yet it's something many farmers don’t pay enough attention to during the renewal season. The deadline to make changes to your APH is April 29th, and this is an opportunity you can’t afford to miss.

Image from Real Ag Stock

What is APH?

At its core, APH refers to the average yield of a specific crop for a farmer over a period of time—typically 4 to 10 crop years. Note the difference between a calendar year and crop year—if a field has been in a 50/50 rotation with corn and soybean for 20 years, you could have yields going back 20 years. Fundamentally, APH is a record of historical crop production that determines how much coverage a farmer can buy under their crop insurance policy. The higher the average yield, the more insurance coverage a farmer is entitled to in the event of a loss.

In essence, APH forms the baseline for calculating coverage. Once an APH is established, other factors can be applied to the database at your agent’s recommendation—these are the “alphabet soup” of letters you may see on a policy (for example, YA = yield adjustment, TA = trend adjustment, YE = yield exclusion). Ultimately, the APH with these adjustments establishes the Approved Yield for a crop. This becomes the backbone of the policy and determines how much is paid in the event of a yield and/or revenue loss on your farm.

Why Reviewing Your 10-Year APH Matters

While it’s easy to focus on the broad strokes of crop insurance—like revenue liability and coverage levels—APH is where the rubber meets the road. It is often overlooked during the renewal season, despite its massive impact on your overall farm.

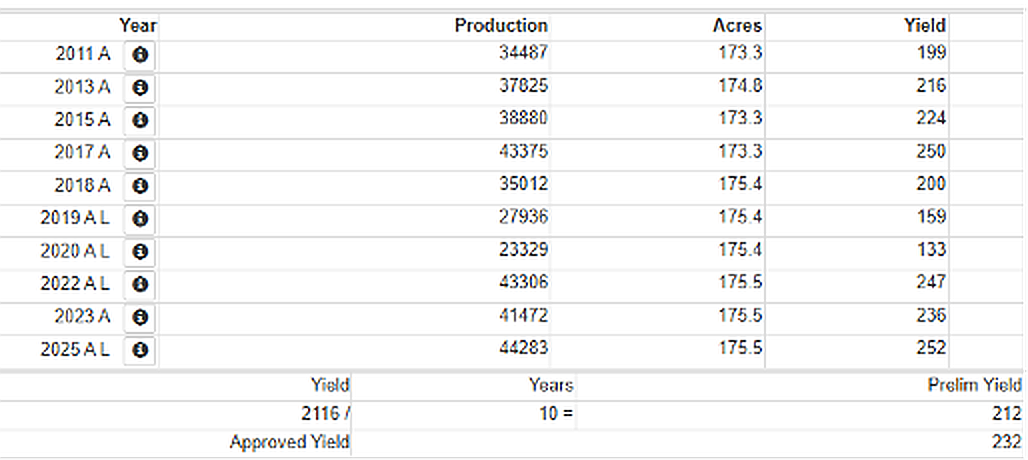

Here’s an example of a corn database for one of our Market Advisor’s family farms

1. Errors in Keying Data

One of the most common problems I’ve seen throughout my career is errors in keying or entering yields into the system. Whether it’s a simple mistake in typing numbers or a more complex error related to new units or farming practices, these issues can have serious consequences. Keying errors are not always easy to catch, especially for processors and underwriters who may not be familiar with the specific production norms of your operation.

For example, look at the database above for 2018-2020. This field in Knox County, IL clearly didn’t respond to years of continuous corn going from 250bpa down to 133bpa. When in the corn and soybean rotation, yields have jumped much closer to 250bpa. This variance shows one-way keying errors happen. Suppose the 250bpa yield from 2017 is mis keyed as 150bpa—which has happened in this field, so it’s something a company underwriter or keying agent could miss. That 100bpa difference would lower the APH on this yield from 232bpa down to about 222bpa. At this year’s spring price of $4.62 per bushel, that’s a loss of $46.20 per acre in protection for a crop you haven’t even planted yet! Even though the system has automated checks for excessively high yields, these checks typically only protect the insurance carrier. Low yields, as in this example, might slip through without triggering an error message, potentially leaving you exposed when you need coverage the most.

2. Impact of New Units, New Counties, and New Practices

Another issue that arises is related to added land and added practices. When you acquire new land or expand to a new county, the system needs to account for those changes accurately. However, mistakes can happen during data entry. For example, are you using the Simple Average (SA) or County Transition (T) Yield for that new tract of land?

Go back to Knox County, IL. The transitional yield for 2026 is 219bpa. Looking at our example, note that the preliminary yield (before adjustments) is 212bpa. Assuming only this unit existed and you added more corn acreage on new land, then the SA would be 212bpa…but if you keyed it incorrectly as in our above example, now it’s closer to 201bpa. Now your new farmland is hurting your claim payout – especially if you have Enterprise Units.

Additionally, if you’re a new producer in a county, you might not be receiving the full county Transition Yield (T) because a simple checkbox wasn’t checked in the system when your policy was set up. These types of overlooked details can make a significant difference in the coverage you receive.

The Risk of Not Reviewing Your APH

This is one hypothetical example resulting in roughly $50/acre of missing coverage. But I’ve seen firsthand how small mistakes in APH data can have a huge financial impact. In some cases, I’ve reviewed policies where a quick clean-up of small errors resulted in an increase of over $100,000 in liability! This could mean the difference between financial recovery and struggling to cover costs after a loss.

Once you file a claim and the payout is based on inaccurate APH data, it’s too late to make changes. Most carriers will not increase policy liability after the acreage reporting deadline.

THE GOOD NEWS: You can update and correct your APH before the April 29th deadline. If you can verify the yields in case of an audit, you can make the changes with your agent.

Key Areas to Review Before the April 29th Deadline

Ensure Accurate Yield Data

Double-check that your historical yield data for the past 10 crop years is entered correctly. Any typographical errors or discrepancies will affect your coverage.Confirm Correct Unit and County Information

If you’ve picked up new acres or expanded into new counties, make sure the correct yields, practices, and transition rules are being appliedCheck for New Producer Status

If you are a new producer in a county, ensure you are receiving 100% if the county T-yield.Look for Underwriting Errors

Take a moment to review your entire policy with a fine-tooth comb. Mistakes, no matter how small, can have a disproportionately large financial impact.

Conclusion: Don’t Wait Until It’s Too Late

I’m not trying to scare you, but I can’t stress enough how important it is to review your crop insurance policy—specifically your APH Database—before the April 29th deadline. The accuracy of your APH data can significantly affect your coverage, and catching errors now could make all the difference if disaster strikes.

Kyle Adams

Crop Insurance Expert | Marketing Advisor, Eastern Corn Belt

With more than a decade of experience as a crop insurance agent, Kyle integrates our marketing strategies with crop insurance products to maximize both sets of tools, creating a well-rounded risk management program for our clients.

Connect with Kyle