All Eyes on January: Will USDA Confirm Soybean Tightness?

Come January, the USDA will release a crucial update detailing Grain Stocks as of December 1, along with revised production figures—often adjusted for acreage and yield. Based on the December WASDE report, soybean carryout projections are already razor-thin, leaving little room for error on paper. Let’s explore why.

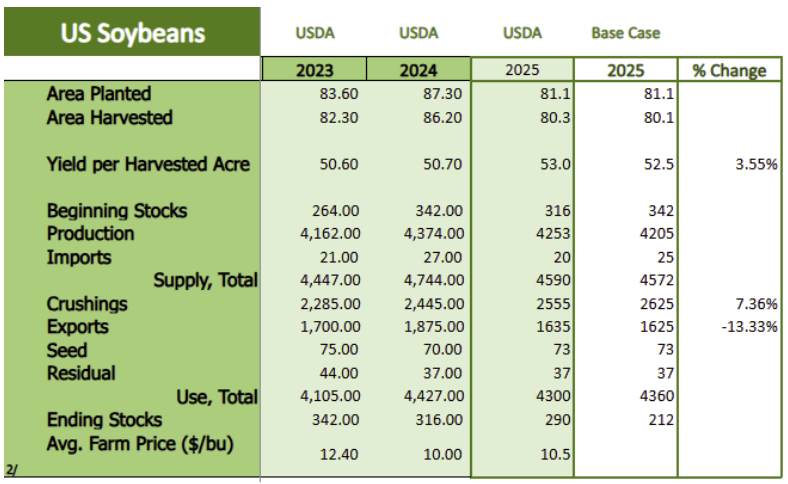

Harvested Acres: Too Optimistic?

I’ve questioned the total corn and soybean harvested acres all year. With CRP (Conservation Reserve Program) acres at their highest since 2013, plus ongoing urban sprawl and clean energy infrastructure growth (solar and wind projects), it’s tougher to justify high acre numbers. Excessive rainfall in key soybean-growing areas, such as North Dakota, central Minnesota, and southern Illinois, only compounds the issue.

Yield Estimates: Don’t Bet the Farm

While USDA yield projections have been trending lower, historical data from the last decade show little consistency in yield changes from October to January. Yield is a toss-up, and given the crop was less than 20 percent harvested when the government shut down, it’s hard to rely on November yield data.

Soybean Crush: Stronger Than Projected

The USDA projected a 4.5% YoY increase in soybean crush as of November, which equals roughly 110 million bushels. But NOPA’s crush data for September and October show a much stronger trend, +11.6% and +13.8%, averaging a 12.8% rise so far. If that pace continues, the USDA would be grossly underestimating domestic demand.

Exports: Elephant in the Room

Exports continue to be the elephant in the room and the focus of most conversations, and for good reason. They’ve been sluggish, which honestly isn’t all that surprising. Total commitments for 2025 trail 2024 by roughly 446.4 million bushels. That said, there’s still time to close the gap, and exports tend to have more room to swing above or below expectations compared to other demand categories. USDA is projecting a 240-million-bushel drop from last year, with about nine months of sales left to reach their 1,625-million-bushel target.

Putting It All Together

Summing it up for argument’s sake:

Cut harvested acres by 200k (ND, MN, Southern IL, KY)

Trim yield by 0.5 to 52.5 bpa (still a record by 0.5 bpa)

Add 5 mb to imports

Reduce exports by 10 mb (though it may be premature to cut beyond 240 mb vs. last year)

Raise crush by 70 mb, aligning closer with NOPA’s 12.8% pace

Even with modest adjustments, you quickly arrive at a scenario where soybean carryout becomes uncomfortably tight.

Prices and the Chart Gap

Does that mean soybean prices can’t pull back, and there isn’t a risk that it all falls apart? Not at all. We’ve seen some price softness recently, with a technical gap near 1060 still looming after a head-and-shoulders breakdown. Managed funds bought heavily this fall and now face decisions about how to position going forward.

The China Narrative and Politics at Play

Why the fixation on whether China will buy or not? I believe it’s twofold:

Political Communication – During the Trump administration, messaging often lacked clarity and accuracy. A more honest and empathetic approach, like “Turning decades of policy takes time and support,” might have done more good than finger-pointing.

Human Nature – As Bob Sorge’s book Dealing with the Rejection and Praise of Man explains, tying self-worth to public opinion is a risky game. Analysts and traders feel pressured to explain every market move, even when there is no meaningful update. Right now, China makes for an easy scapegoat.

Bottom Line

It doesn’t take extreme scenarios to argue that soybean supply could tighten quickly. While export headlines may dominate the narrative, fundamentals like acreage, yield, and crush trends point toward a market on edge. Watch for major shifts after the January USDA update—this one could move the needle.

Garret Brown

Founder | Market Advisor

Having grown up on a farm, Garret respects the wide range of skills needed to run a successful operation and recognizes farmers are often stretched thin trying to do it all. This understanding, along with his affinity for markets, fuels his drive to make tough marketing decisions simpler for farmers.

Leveraging his experience in grain origination and margin management, Garret analyzes technical and fundamental market information. With the assistance of CODAK’s algorithmic signaling platform, he puts together buy/sell recommendations while working with the CODAK team to create strategies that accommodate each farmer’s personal risk tolerance, on-farm storage capacity, and break-evens.